Financial Tools

Use Corcoran Consulting Group’s Financial Model to Calculate Gross Profit

05/26/2023

Our previous blog post recommends four strategies home health organizations can use when negotiating with Medicare Advantage providers. Here, we offer a useful worksheet to help you with Strategy #3 - calculating your gross profit by discipline and by payer.

Click here or on the worksheet image below to open and download our Payer Analysis and Gross Profit Financial Management Model worksheet. After opening the link, select File, then “Save As” to save a copy to your computer’s desktop.

*This worksheet is designed to be informational only. The estimated values shown are hypothetical and are provided for illustration purposes only. There are many factors which affect gross profits for your home care business including, among other considerations, geographic area, overall size, quality of earnings and timing. You should consider the counsel of certified financial, operational and clinical professionals in home health care before making any decisions.

Instructions & Information to use the Gross Profit Management Model

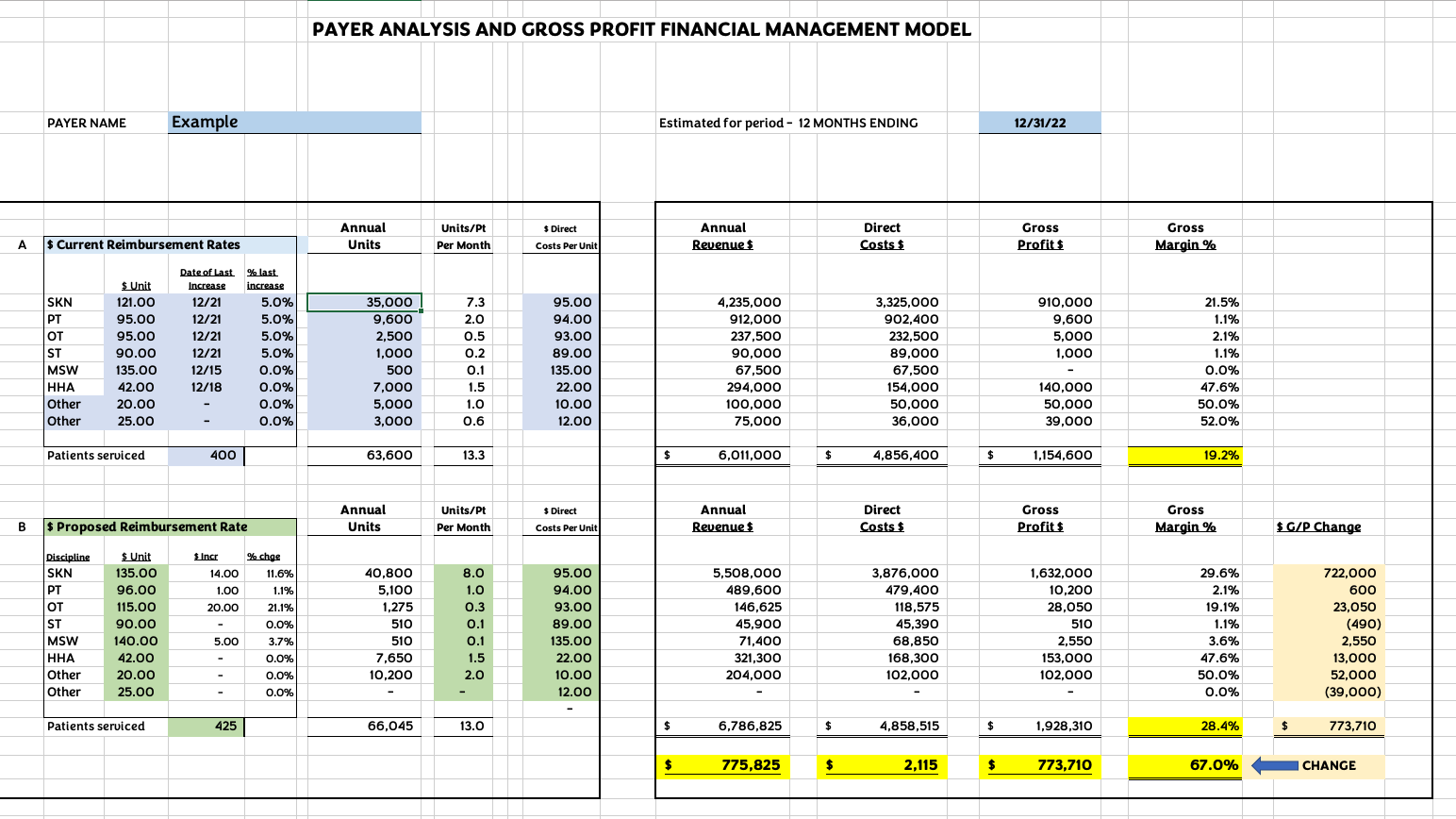

A. Current Situation

1. Enter current reimbursement rates by discipline in the block labelled "A".

2. Enter the number of patients served annually (this should correlate with the number you use in #4 below.

3. You can, although not necessary, enter information about last increase dates and %'s for your information when negotiating.

4. Enter total units (visits, hours, etc.) in the space for each discipline. You have the option of inserting the actual number of visits, units or what you project in the next year, etc. In any event, use an annual number.

5. From your latest cost report in section "Worksheet A, Column 10", take the cost by discipline and divide by the visits in "Worksheet S-3, Total Visits by discipline", and enter the direct costs for each discipline. IF you have better more current information on direct costs, use it instead of the cost report information.

B. Proposed Change

1. In the "Proposed Reimbursement Rate" block, enter what you would like to achieve in a reimbursement increase negotiation with the Payer. You should try to be strategic in your approach to the negotiation. If you do very little of a particular discipline, you should put less focus on an increase; focus, instead, on that discipline which will make the most significant improvement in your overall gross profit with this Payer.

2. Enter the planned changes in annual units, direct cost change, if any, and the patients expected if a possible change is likely.

3. Based on your reimbursement "strategy", you may wish to increase or decrease your utilization to provide the best care while improving your overall margin. You can adjust the utilization in "Units/Pt" column.

C. Analysis

1. First, note your current gross margin for this payer, highlighted in yellow to the upper right of the worksheet. This number MUST be greater than 0.0%. In fact, each of the percentages above this number must be positive for each discipline. If not, every time you do a visit, you lose money.

2. Review the Annual Revenue, Gross Profits by Discipline on the right side of the worksheet. If you have any margins that are negative, and the dollars are other than insignificant, this is potentially an area to look for an increase in reimbursement.

3. Review the Gross Profit column and look for the disciplines where you have the most dollars of revenue and where the gross margin is less than desired (e.g. 30% ). This represents a discipline where a change (perhaps even a small change in reimbursement rate) will be material to your company.

4. To the bottom right of the first page of this analysis, you will see the "Gross Profit" $ Change by discipline for this payer. Your gross profit improvement strategy can be designed by working with the "Proposed Reimbursement Rates" and potentially improved by managing the utilization or "Units/Pt Per Month" column, and possibly by improving upon your direct expenses with improved productivity, etc. In addition, you may determine that there is a certain patient type that you will add or no longer service, thereby changing the units, utilization and number of patients served.

5. The goal of the financial model is to allow you to "massage" your reimbursement rates and costs by discipline so that the overall gross profit and margin improves. And that it improves to such a degree that it is higher than the gross profit you need to break-even and make a bottom line profit. Compare the Gross Margin % in the upper right corner to the section below marked "CHANGE"

6. Other statistical information is included on the second page for your use in examining the changes you are proposing.

Definitions

Direct Costs - Direct costs are those costs that are directly incurred for each visit to a patient. These costs include the clinician/caregiver payroll cost (or contracted cost), benefits, payroll taxes, mileage/transportation and supplies used. Every time you make a visit to a patient, this cost will increase and directly relative to the number of visits.

Reimbursement Rate - This is the rate that the payer will reimburse you for each visit for a specific discipline. This amount MUST be higher than the Direct Cost.

Gross Profit - The dollar amount remaining after Direct Costs are deducted from the Reimbursement Rate. E.g. $100.00 reimbursement rate less direct cost of $82.00 equals gross profit of $18.00

Gross Margin - This is the percentage of Gross Profit $ to the Reimbursement Rate. In the above example, this would equal 18% ($18.00 / $100.00).

Total Gross Profit - Your total gross profit dollars must be greater than your "overhead/all other expenses" so that your company will have a "bottom line" profit. If your gross profit is not more than all other expenses, you will have a bottom line loss.

Overhead/ All Other Expenses / Operating Expenses - All other expenses of operating your business excluding the Direct Expenses. Think of expenses as two types – "Direct" and "All Other". All Other expenses are those that you will incur solely by operating your business each day/month. These expenses include executive and management payroll, their taxes and benefits, insurances, rent, IT, office administrative staff, professional fees, etc. etc. These expenses do not change in proportion to visits unless there is a dramatic change in overall business operations. They do increase or decrease based on management decisions, increases in the cost of expenses, adding/decreasing certain programs or the method in which some expenses can be managed (outsourcing, etc.).

EBITDA - A sort of fancy term that means Earnings Before Interest, Taxes, Depreciation and Amortization. It also simply equates to "Operating Income" or "Income from Operating Activity." As the term is defined, it excludes the "non-operating" type of costs related to non-cash expenses, financing costs, taxes. Think of this term or "Operating Income" as your earnings from the company activities of visiting patients less the real costs of all activities associated with running the company.

Break Even Point - If you would like to know how much revenue you need to have so that you "break-even" from operations, you would take all of your "overhead/all other" expenses and divide that by your gross margin %. This will equal the revenue you need at that gross margin % to cover all of the other expenses.

Want a dialed-in picture that takes into full account your agency’s operational, financial, and clinical situation? Contact Maryanna Arsenault at ma@corcoranconsultants.com for a confidential, no-obligation chat.

Are you ready?

Sign Up For Our Monthly Insights

Sign up for our e-newsletter and receive valuable insights for your care at home organization.

Schedule An In-Person Meeting

For those who are ready to meet face to face, and talk seriously about analyzing the financial operations of their agency.

Schedule A Virtual

Meeting

For those who aren't ready to meet face to face in-person but want to talk seriously about the financial operations of their agency.